Articles

Expanding low-carbon H2 use in European industry

OPENING PHOTO: Under a €275-MM, 4-yr project, Total revamped its former oil refinery in southeastern France to produce 500,000 metric tpy

of biodiesel and biojet. The Masshylia project will produce green H2 for use at the biorefinery. Photo copyright Total and François Lacour.

As part of the EU’s Strategy for Energy System Integration under the European Green Deal, low-carbon H2 is being promoted as a solution for those sectors where electrification is difficult. More specifically, the EU’s Hydrogen Strategy, which was unveiled in July 2020, calls for large-scale deployment of clean H2 at a fast pace as a key part of the EU’s strategy to cost-effectively reduce greenhouse gas (GHG) emissions by 50%–55% by 2030. This will involve the installation of at least 6 GW of renewable H2 electrolyzer capacity in the EU by 2024 and 40 GW by 2030.

To this end, the EU’s Hydrogen Strategy estimates that cumulative investments in European green H2a could amount to €180 B–€470 B ($215 B–$562 B) by 2050, and to €3 B–€18 B ($3.5B–$21.5B) for low-carbon H2 and blue H2.b According to the EU report,1 analysts estimate that clean H2 could meet 24% of global energy demand by 2050, with annual sales as high as €630 B ($754 B).

Notwithstanding these predictions, the use of H2 on a wide scale faces several hurdles, chiefly:

- A large-scale infrastructure buildout, requiring a critical mass in investment and cooperation among corporate and country partners

- The development of an enabling regulatory framework for H2 markets and source certification

- Technology breakthroughs to offer new solutions for producing, using, storing and transporting green molecules

- A significant scale-up in renewable power capacities

- Necessary, further reductions in H2 production costs

The price of decarbonization In line with its net-zero carbon goal, the EU plans to prioritize green H2 production, mainly from wind and solar energy. Over the short-term and medium-term, however, blue H2 will be needed to rapidly reduce emissions from existing gray H c production and support the parallel and future development of green H2 production.

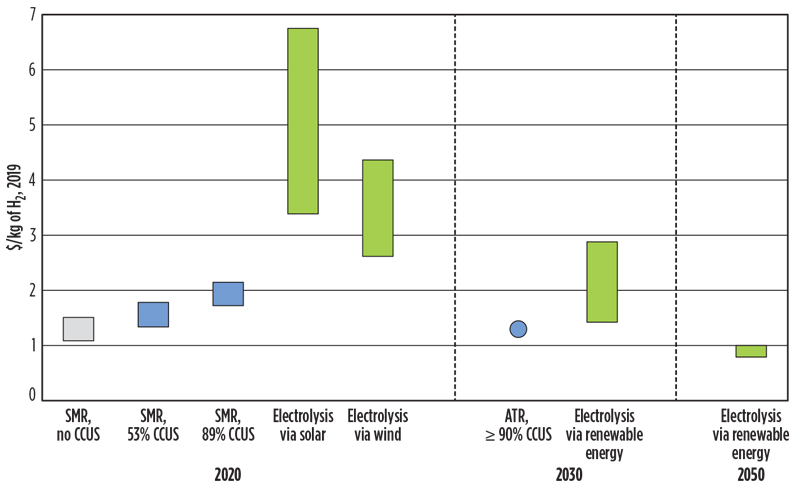

Feeling blue? The success of blue H2 use will be largely dictated by prices for both carbon capture and natural gas. At present, the cost of producing blue H2 increases in parallel with increasing rates of CO2 capture (FIG. 1); however, as infrastructure expands and the cost of CO2-capture equipment decreases, blue H2 production costs are anticipated to fall over the next decade. A transition from steam methane reforming (SMR) to au- to thermal reforming (ATR), which combines process and combustion emissions, could push the cost of blue H2 production to $1.25/kg (€1.05/kg) of H2 by 2030.

Fig. 1. Present and projected costs for different types of H2 production, 2020–2050. Note: Gray H2 and blue H2 assume a natural gas price of $3.50/MMBtu.2

At present, carbon capture and storage typically adds $50/t (€42/t) of CO2 captured to the cost of producing blue H2, or $0.25/kg (€0.21/kg) of H2 to the cost of gray H2. If less concentrated CO2 is captured from exhaust gases, this adds $0.40/ kg (€0.33/kg) of H2 to the cost of blue H2, with an emissions abatement cost of more than $100/t (€83/t) of CO2.2 Additionally, natural gas prices are forecast to increase, which could drive up costs for blue H2 production by nearly 60% by 2040, according to Wood Mackenzie.3

Seeing green. Conversely, Wood Mackenzie predicts that green H2 production costs could fall by as much as 64% by 2040 with greater utilization and reduced renewable power prices, at which time the cost of green H2 will equal the cost of fossil-based H2.3 In some European countries with numerous green H2 projects, such as Germany, green H2 costs will be at or near parity with fossil H2 costs closer to 2030.

Costs for electrolyzers for green H2 production are expected to decrease by 50% between 2020 and 2030 with improved economies of scale, after already decreasing by 60% between 2010 and 2020. By 2050, electrolyzer costs may decline by as much as 90% from present- day price levels. This anticipated cost decrease and manufacturing scale-up will allow green H2 in areas where renewable power is inexpensive to compete with fossil-based H2 by the start of the next decade. It will also aid the EU’s effort to install 40 GW of electrolyzer capacity to produce up to 10 metric MMt of renewable H2 in the EU by 2030.1

Between 2030 and 2050, renewable H2 technologies should reach maturity and be deployed at large scale in the EU to reach all difficult-to-decarbonize sectors. In this period, renewable electricity production must be massively increased, since nearly 25% of renewable electricity could be dedicated for renewable H2 production by 2050.

Expansion of H2 markets in Europe. As H2 infrastructure and production expands, H2 will find application in a number of new areas. It can be used to decarbonize steelmaking and mining operations, as well as for fuel in truck, rail, marine and other transportation modes. Green H2 can be stored as back- up power for renewables-based energy grids, providing flexibility and reliability of supply.

Furthermore, with some retooling of infrastructure, H2 also can be used in residential and commercial heating, which accounts for a large amount of CO2 emissions in cold climates. A demonstration project in Fife, Scotland will heat 300 homes from late 2022–March 2027 with 100% green H2 from a purpose-built H2 system. Offshore wind energy will be used to power the electrolyzer to produce the H2 for the H100 Fife project. Other pilot projects are ongoing to analyze the potential to replace natural gas boilers with H2 boilers.

The creation of new end-use markets is key to scaling up the production of H2. A primary market is industrial applications. In industry, one of the most immediate applications for low-carbon H2 is to reduce and replace the use of emissions- intensive gray H2 in refineries. Although most project announcements within the last couple of years have focused on green H2 substitution, some blue H2 initiatives are seen in Europe.

Blue H2: A bridge to green. The EU’s Hydrogen Strategy estimates that carbon prices would need to be €55/metric t–€90/metric t of CO2 to make blue H2 competitive with gray H2 today. However, the strategy also notes, “...the further retrofitting of existing fossil-based hydrogen production with carbon capture should continue to reduce greenhouse gas and other air pollutant emissions in view of the increased 2030 climate ambition.”1

In light of this provision, some European countries have taken steps to incorporate fossil-based and blue H2 into their overall clean energy and H2 strategies. Germany’s National Hydrogen Strategy leaves room for fossil-based H2 with carbon capture as a bridge to longer-term use of green H2, noting, “The Federal Government believes that both a global and European hydrogen market will emerge in the coming 10 years and that carbon-free (for example, blue or turquoise) hydrogen will be traded on this market.”4 Germany has committed €7 B ($8 B) of funding to develop its early-stage H2 industry.

Although it no longer abides by EU policy, the UK government’s climate change advisory body has expressed support for blue H2 as a means of quickly scaling up the H2 economy in tandem with green H2 projects. Studies suggest that H2 generated from renewable energy and natural gas could provide more than 45% of UK total energy demand by 2050—without the financial crutch of direct subsidies, but with coordinated policy support across the H2 supply chain. UK project developments. A few blue H2 projects are already in progress in the UK. Equinor is leading a 600-MW ATR blue H2 project at Saltend Chemicals Park in the Humber region called H2H Saltend, with FID expected in 2023. The project would reduce emissions from the site by nearly 900,000 metric tpy of CO2. H2H Saltend will also form part of the Zero Car- bon Humber project, a collaboration with National Grid and Drax Power to export carbon-neutral power and H2 to industrial centers in the east of England by 2040.

Meanwhile, Essar Oil UK is working with Progressive Energy Ltd. to install a blue H2 project at its 204,000-bpd Stan- low refinery in northwest England. The initial phase will produce 3 TWh/yr of blue H2 via SMR by 2025, with a later expansion to 9 TWh/yr. Progressive Energy has been working with several UK companies to switch industrial operations to low-carbon H2 through existing gas networks. The Essar Oil project is part of that wider initiative, called HyNet, which received £7.48 MM in funding from the UK government in 2020.

Industrial integration of green H2. SMR produces approximately 10 metric t of CO2 for each metric t of H2 produced. Half of these emissions are linked to fossil feedstock use. A medium-size conversion refinery consumes around 50 kilotons/yr of H2, and the SMR process accounts for approximately 30% of the plant’s H2 production.5

Worldwide, dedicated H2 production emits 830 MMt of CO2, which accounts for more than 2% of fossil CO2 emissions at present.2 On-purpose H2 production accounts for about 15% of emissions associated with the European refining industry as of 2018, including CO2 coming from SMR and fuel use. To completely replace the 50 kilotons/yr of H2 used in these refining processes would require an installed electrolyzer capacity of around 340 MW with an average energy consumption of 2.5 TWh/yr–2.75TWh/yr.5 Electrolyzer utilization of just 40%–45% can achieve a significant reduction in refinery H2 production cost.

Several collaborative decarbonization projects are taking place between energy majors and power producers to integrate green H2 production into fuel production by partially replacing gray H2 use, there- by offsetting CO2 emissions. A review of these projects and their significance for the development of Europe’s H2 sector is detailed in the following sections.

REFHYNE at Rheinland. The €16-MM REFHYNE project at Shell’s 160,000-bpd Rheinland oil refinery in Wesseling, Germany is led by a consortium of Shell, ITM Power, SINTEF, thinkstep AG and Element Energy, and funded by the Fuel Cells and Hydrogen Joint Undertaking (FCH JU). The project is building a large proton exchange membrane (PEM) electrolyzer, a 10-MW plant from ITM Power, to produce 1,300 metric tpy of H2 for use at the refinery. The project will run for 5 yr through December 2022.

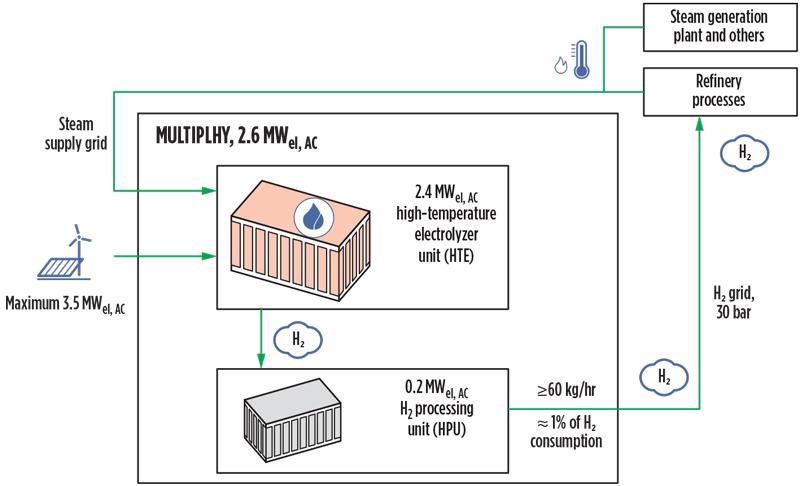

MULTIPLHY at Rotterdam. The MULTIPLHY project at Neste’s 800,000-metric-tpy biodiesel refinery in Rotterdam, the Netherlands is the world’s first multi-MW-scale, high-temperature, solid oxide electrolyzer (SOE) project for efficient H2 production in an industrial biofuel refining process. The project, which is led by a consortium that includes project engineer and stakeholder Engie, aims to produce 960 t of green H2 by the end of 2024, thereby avoiding the emission of 8,000 t of GHG emissions. The 2.4-MW SOE, provided by Sunfire, will have a nominal power input of 2.6 MW and an H2 production capacity of 60 kg/hr, making it at least 20% more efficient than a conventional, low-temperature electrolyzer (FIG. 2).

Fig. 2. The MULTIPLHY project’s solid oxide electrolyzer will have a nominal power input of 2.6 MW and an H2 production capacity of 60 kg/hr, making it 20% more efficient than a low-temperature electrolyzer. Image source: MULTIPLHY Project EU.

Lingen Green Hydrogen. The Lingen Green Hydrogen project at BP’s 100,000-bpd oil refinery in Lingen, Germany is a collaboration with wind power developer Ørsted, slated for startup in 2024. Wind power from Ørsted’s North Sea wind farm is planned to generate the power for 9,000 tpy of H2 production from a 50-MW electrolyzer, which would replace 20% of the natural gas-based H2 used at the refinery and avoid 80,000 metric tpy of CO2- equivalent emissions.

The planned project is a step toward BP’s promise to reduce its fossil fuel production by 40% through 2030 and increase its investment in sustainable energy solutions. BP will take a final investment decision (FID) on the project in 2022, depending on EU funding. The project is also intended to support a longer-term ambition to build more than 500 MW of renewable-powered electrolyzer capacity at Lingen.

Masshylia in France. The Masshylia project at Total’s 500,000-metric-tpy Le Mède biorefinery in France (OPENING PHOTO) is a JV between Total and Engie to design, develop, build and operate an H2 production site, powered by solar farms with a total capacity of more than 100 MW. The 40-MW electrolyzer will produce approximately 1,825 metric tpy of green H2 to meet the needs of the plant’s biofuel production process and simultaneously avoid 15,000 metric tpy of CO2 emissions.

A large-scale solution for H2 storage will be implemented to manage the intermittent production of solar electricity and the biorefinery’s need for continuous H2 supply. Construction is slated to start in 2022, with operation targeted for 2024. Beyond this first phase, new renewable farms may be developed by the partners for the electrolyzer, which will have the capacity to produce up to 5,500 metric tpy of green H2.

Westküste 100 in Germany. The 30- MW pilot phase of the planned, 700-MW green H2 project at Raffinerie Heide’s re- finery in Schleswig-Holstein, Germany is under construction by the H2 Westküste JV comprising EDF Deutschland, windpower developer Ørsted and independent refiner Raffinerie Heide. If the €89-MM, 5-yr pilot phase is successful then the JV will move forward with its 700-MW electrolyzer project to produce H2 for nearby cement manufacturing and local residential heating.

A large percentage of the green H2 would be combined with CO2 captured from the cement plant to produce synthetic methanol, which would then be refined into synthetic jet fuel for use at the Hamburg airport. Some of the green H2 would also be used as fuel for local transportation. Additionally, up to 10 metric MMt of H2 could be stored inside salt caverns on the Heide refinery’s land, and transported on an existing, bidirectional H2 pipeline to a nearby Linde facility for distribution.

Foundations for green growth. Although these green H2 industrial projects are at limited scale and will not produce enough H2 to meet the refineries’ total H2 requirements, they are important demonstration projects to show what is possible for the future of H2 in European industry. Funding is a necessity for such projects, as nearly all of the ventures detailed here have incorporated EU funding into their feasibility studies.

“These projects are critical for moving green H2 to an industrial level, but at the moment they need support,” commented Joris Mertens, Principal Consultant at KBC, A Yokogawa Company, on an H2TechTalk podcast in early February. “But one of the ways to reduce the cost of green H2 is scaling up to reduce the investment cost. One main cost factor is the cost of power, and the other is electrolyzers, which will be getting cheaper with novel technology and larger scale,” Mertens explained.6

Similarly, a 2018 technical report from the European Commission’s science and knowledge service, the Joint Research Center ( JRC), stated that, “Following expected general techno-economical developments, with more and more renewable energy introduced and distributed by a larger, more efficient grid, the fraction of green hydrogen used in fuel refining will have the opportunity to grow and, depending on the scenario considered, potentially reach a steady maximum around 2050.” 3

However, the JRC report also noted, “The recognition of the role green hydrogen can play, and legislation introducing a clear methodology, such as mass balancing to account for its use in refining processes, is needed to support its introduction. It is anticipated that regulations other than the EU European Trading Scheme (REDII, for example) will offer higher incentives and, there- fore, will be more relevant for the industry than those associated with the European Emissions Trading Scheme.”

As regulatory and market frameworks are further developed and refined for H2 (e.g., the FCH JU’s CertifHy Guarantee of Origin EU-wide program for green H2), demand for low-carbon and zero- carbon H2 will continue to grow. European industry’s commitment to becoming a net-zero emitter of CO2 by 2050, in line with EU climate goals, will result in a marked increase in European production of clean and renewable energies and energy carriers, including H2. In line with this increase, greater substitution will be seen of green H2 for gray H2 in industrial processes, as well as increased utilization of CO2 capture in methane reforming to produce blue H2 for industrial use.

NOTES

a “Green” H2 is produced from electrolyzers that are powered by zero-emissions renewable energy.

b “Blue” H2 is produced from the reforming of methane, with the resulting CO2 captured and stored to offset environmental impact.

c “Gray” H2 is produced from the reforming of methane and does not include CO2 capture—i.e., the most common type of H2 used in industry.

LITERATURE CITED

1 European Commission, “A hydrogen strategy for a climate-neutral Europe,” July 7, 2020, Brussels, Belgium.

2 Bartlett, J. and A. Krupnick, “The potential of hydrogen for decarbonization: Reducing emissions in oil refining and ammonia production,” Resources, February 4, 2021.

3 Wood Mackenzie, “Green hydrogen costs to fall by up to 64% by 2040,” August 25, 2020.

4 German Federal Ministry for Economic Affairs and Energy, “The national hydrogen strategy,” Berlin, Germany, June 2020.

5 Dolci, F., “Green hydrogen opportunities in selected industrial processes,” European Commission Joint Research Center, Technical Report. June 20, 2018. Brussels, Belgium.

6 H2TechTalk, “Optimizing and decarbonizing industrial hydrogen supply,” Podcast interview with Joris Mertens, February 2, 2021, Online: https:// blubrry.com/h2techtalk/73352437/optimizing- and-decarbonizing-industrial-hydrogen-supply

Related Articles

Connect with H2Tech