Articles

Emissions-free production of blue H2 for efficient transportation and decarbonization

T. R. REINERTSEN, REINERTSEN New Energy, Trondheim, Norway

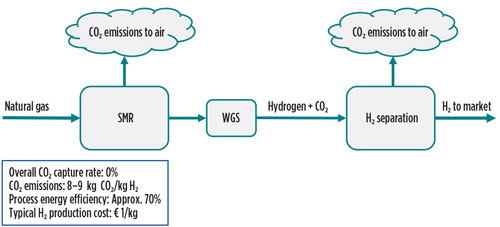

Hydrogen production from gas, oil and coal has a reputation for being dirty and inefficient. At present, the majority of the world’s H2 is produced and used in oil refineries and chemical plants. Large emissions of CO2 and other gases come from two main sources in these plants—steam methane reforming (SMR) and the downstream treatment of the synthesis gas, or syngas (FIG. 1).

Fig. 1 Conventional production of gray H2 (high emissions).

Existing plants may be retrofitted to capture CO2 from reformer flue gas and by separating CO2 from syngas. However, the overall CO2 capture rate will be lower than 90%, and the costs of these methods are generally high.

Over the last few years, the industry has developed new process solutions for H2 production. In these new concepts, SMR is often replaced by autothermal reforming (ATR), with no direct emissions to the atmosphere. However, CO2 emissions from the overall process are still at least 5%–10%.

Zero-emissions blue H2

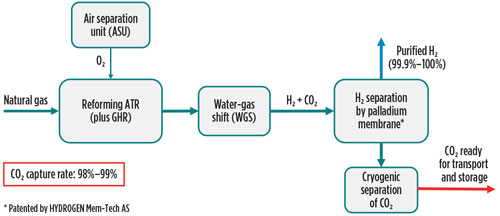

REINERTSEN New Energy has developed a new process, HyPro-Zero, that gives H2 production with close to zero emissions. The process is based on existing technology in a new process flow (FIG. 2). It encompasses ATR and, optionally, a gas-heated reformer (GHR) fed with O2.

Fig. 2 A new process for large-scale, emissions-free production of H2. Patent pending by REINERTSEN New Energy.

Following the water-gas shift (WGS), the syngas is separated by palladium membrane technology. The palladium membrane separator is developed by subsidiary HYDROGEN Mem-Tech AS. The HyPro-Zero process achieves a very high CO2 capture rate of 98%–99%. The purified H2 produced complies with fuel cell quality requirements. The CO2 is produced by cryogenic separation to a quality standard that is ready for transportation and storage.

Competitive H2 production

The HyPro-Zero process facility is projected to have a reduced CAPEX of 25% compared to existing process solutions. The production cost for H2 from natural gas is estimated at €1.5/kg H2–€1.7/kg H2, based on a natural gas price of €0.12/sm3 and including the capture, transportation and storage of CO2 (TABLE 1).

This cost estimate is significantly less than other solutions available. At present, blue H2 can be produced at a cost of 50% or less than the cost of green H2 via electrolysis with renewable power. The gas energy efficiency is high, at approximately 80%. Furthermore, blue H2 can be produced at much higher volumes than green H2—typically 100 times more per plant.

CO2 storage

Available CO2 storage or utilization is a prerequisite for the production of emissions-free blue H2. CO2 is stored onshore and offshore in Norway, the U.S., Canada and several other countries.

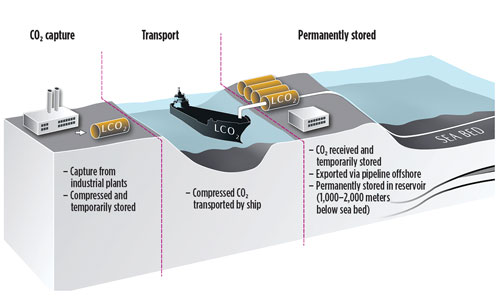

Recently, Norway decided to build a large CO2 storage facility, referred to as the “Northern Lights” project (FIG. 3). CO2 captured from industry and blue H2 production facilities in Norway and other European countries will be transported by ship or pipeline to a CO2 terminal on the coast of Norway. From the terminal, the CO2 will be piped offshore and then injected into a subsea reservoir. The initial investment and operation costs for the Northern Lights project are estimated at €2.5 B.

Fig. 3 Northern Lights CO2-capture project details. Source: Equinor.

Transportation of H2

A major challenge for the market penetration of H2 is the high cost for distribution and storage. Compressed and liquified H2 contained in tanks is not very cost-efficient due to the low density of H2. Decentralized, small- and medium-scale production of green H2 might be advantageous in such cases.

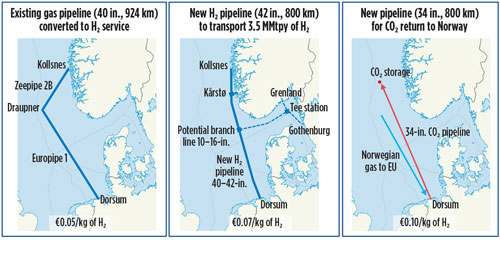

However, centralized, large-scale, blue H2 production and transportation in large-diameter pipelines is very cost-efficient. As an example, the author’s company has studied the production of blue H2 for the European market, based on Norwegian natural gas. The study examined whether the H2 should be produced in Norway close to CO2 storage and then transported in existing or new gas pipelines, or if the H2 production plant should be located close to the market and the CO2 returned to a storage facility. Three alternatives are illustrated in FIG. 4.

Fig. 4 Example costs of gas pipelines for efficient H2 transportation.

The option on the left in FIG. 4 shows an existing pipeline, Zeepipe 2B/Europipe 1 (40 in., 924 km), redesigned from natural gas to H2 service. The middle option shows the construction of a new, 42-in., 800-km H2 pipeline to transport 3.5 MMtpy of H2. The option on the right assumes a large-scale H2 plant based on Norwegian gas, placed in the Netherlands or Germany, along with a CO2 return line (34 in., 800 km) to a Norwegian storage facility.

Estimated costs for the three alternatives show that the cost of transporting large volumes of H2 to the EU is very low for all cases, at less than €0.08/kg H2. Estimates for the pipeline transportation cost are based on a novel H2 pipeline design that allows the use of existing subsea pipelines with a minor reduction of design pressure. The author’s company carried out the original design of the Zeepipe 2B gas pipeline and used this knowledge to theoretically redesign the subsea pipelines for high H2 pressure and flow. Other European studies indicate approximately the same potential for H2 distribution networks.

The total production and transportation cost for Norwegian blue H2 to Europe is estimated at approximately €1.7/kg of H2. Although some costs (financing costs, contingency costs, etc.) are not factored, the estimated result promises a competitive, clean energy solution for the energy transition in Europe and elsewhere.

Major markets for blue H2

Future markets for blue H2 solutions are regions with access to natural gas and geology for CO2 storage. Other regions that presently import fossil energy may be importing H2 in the future. Long-distance pipeline transportation of H2 might be an option for these areas.

The major markets for blue H2 solutions with long-distance pipelines are Europe, the U.S., Canada, Australia, the Middle East, Japan, South Korea and, to an extent, Southeast Asia. Some countries, like China, prefer to use coal as a source for H2 production. In principle, this is a viable option since coal is cheap, but the CO2 emissions volume to be handled is about twice as great as for natural gas. Furthermore, the cleanup prior to gas reforming is extensive.

Based on 2020 reports1,2 by the International Energy Agency and Concawe, the author’s company has estimated the major users of blue H2 solutions. The main market segments for blue H2 include:

- Direct use, ammonia and e-fuel

- Biofuel production

- H2for carbon capture, storage and utilization in industry.

Considering the uncertainties and sustainability issues connected to e-fuel and biomass, the estimates indicate a need for the startup of a world-scale blue H2 plant every two weeks, globally, from 2030. A world-scale blue H2 plant would produce approximately 400,000 tpy of H2. The need for CO2 storage would be 8 t–10 t of CO2/t of H2.

Reduction of CO2 emissions

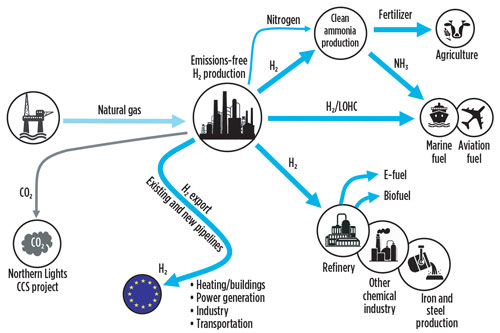

Emissions-free blue H2 may be used to efficiently produce clean fuels or to cut CO2 emissions from power generation, buildings and industry, as shown in FIG. 5.

Fig. 5 H2value chains.

Blue H2 may also be a competitive pre-combustion alternative to post-combustion carbon capture from flue gas (exhaust). By replacing natural gas with low-cost, emissions-free blue H2 in industrial processes, very competitive CO2 abatement costs may be realized. Also, the total CO2 emitted will be less due to the high cost of capturing the last fractions of CO2 from flue gas with the use of amine, etc. (10%–20%).H2T

LITERATURE CITED

1 International Energy Agency, “Energy technology perspectives,” September 2020.

2 A. Soler, under supervision of M. Yugo, “Role of e-fuels in the European transport system—Literature review,” Concawe Low Carbon Pathways Joint Group and Concawe Fuels and Emissions Management Group, January 2020, Online: https://www.concawe.eu/wp-content/uploads/Rpt_19-14.pdf

TORKILD R. REINERTSEN is Chairman and Market Lead for Hydrogen at REINERTSEN New Energy AS in Trondheim, Norway. Dr. Reinertsen has been delivering engineering and EPC projects to oil and gas companies for 30 yr. At REINERTSEN New Energy, he focuses on solutions and technologies for clean and efficient H2 production with carbon capture and storage. He also specializes in complete value chains for H2, H2 carriers and clean fuels. Additionally, Dr. Reinertsen is the Founder of HYDROGEN Mem-Tech, which has developed efficient palladium membrane technology for the separation of H2 from gas mixtures.

Fig. 1. Conventional production of gray H2 (high emissions).

Fig. 2. A new process for large-scale, emissions-free production of H2. Patent pending by REINERTSEN New Energy.

Fig. 3. Northern Lights CO2-capture project details. Source: Equinor.

Fig. 4. Example costs of gas pipelines for efficient H2 transportation.

Fig. 5. H2 value chains.

Related Articles

Connect with H2Tech