Articles

Manage the new risk profile of energy transition projects

Infrastructure and Distribution

M. REEVES and C. PORTILLO, TritenIAG, Houston, Texas; R. BORGH, TritenIAG, Seattle, Washington

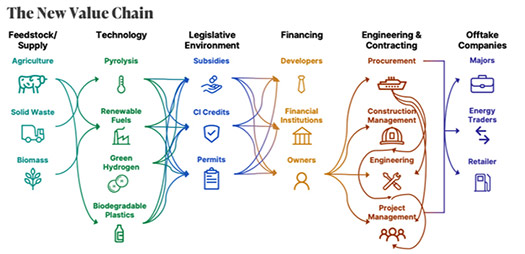

The time is ripe to realize the vision of a clean energy future. However, that future comes with new risks. In the old era of vertical energy integration, a few companies controlled the value chain—from crude oil to product retail. Major energy companies owned the oil and gas in the ground and proprietary processing technologies, exerting major influence over the regulatory process. They had a balance sheet to pay for their projects, worked with their preferred engineering, procurement and construction (EPC) firms and owned the retail organizations to distribute products to consumers (FIG. 1).

The new value chain is comprised of stakeholders that historically have never worked together. Instead of crude oil, feedstocks are sourced from nature, agriculture and waste management companies. Each process requires novel and adapted technologies offered by different vendors with competing guarantees. Early economic incentives exist via the U.S. Renewable Fuel Standard market program, low-carbon fuel standard credits and U.S. Inflation Reduction Act; however, the regulatory environment fluctuates. Developers with little experience in major complex projects must now navigate financing challenges, conflicting EPC approaches and entrenched product retailers (e.g., offtakers).

These factors add up to a new project risk profile. Three areas are critical to managing new project profile risks: project definition, technology selection and stakeholder requirements.

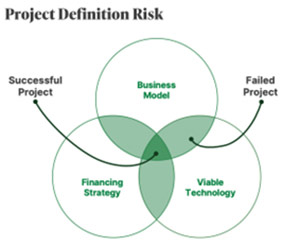

Project definition. Projects in the new value chain must optimize three inputs in project definition: the business model, the financing strategy and the viable technology. Aligning only two of these inputs will not result in a successful project (FIG. 2).

First, a sound business model must be established. In addition to balancing feedstock and the product market, a proper business model requires favorable yield structures, balanced operating costs and a realistic total installed cost. Concurrently, the money must be available to pay for the project, whether it is debt, equity, cash flow or a combination of all three (FIG. 3).

Technology selection. The project definition will drive technology selection, and the chosen technology path will impact carbon intensity. Many competing technologies may meet the same project goals. For example, at least four competing hydroprocessing-based technologies produce renewable diesel from vegetable oils and animal fats, and there are at least three feed pre-treatment options.

As with anything untried, novel technologies introduce risk; however, with risk comes the potential for reward. Conducting detailed due diligence, taking the time to understand the technology and negotiating guarantees will mitigate some of this risk.

Stakeholder requirements. Today’s sustainable projects have new stakeholders—financial institutions, project developers and startups—that may have never executed a complex project. These stakeholders may lack a nuanced knowledge of technology, schedule or escalating costs, which means risk. With risk comes the need for guarantees from the technology provider and EPC firms. These can be guaranteed lump sum pricing or an overall financial and technical wrap. This passes risk on to the EPCs, which are not always willing to accept the risk; other stakeholders, including banks and owners, may have to contribute more equity.

Stakeholders must understand the importance of efficient execution and achievable schedules in meeting deadline-critical government incentives. The historical project scheme may not be acceptable in today’s world, where time to market is critical. Compressed engineering schedules can shorten the engineering time and help identify long lead equipment early in the design engineering phase. A fast-track project will require overlap in the front-end loading (FEL)-2 and FEL-3 phases and detailed design and construction.

Takeaway. Overall, energy transition projects have a fragmented value chain, competing and new stakeholders, and a complex technology selection process. Project risk can be reduced and return on investment (ROI) maximized with accurate project definition, compressed delivery schedules and expert management.

Two essential factors drive energy transition projects:

- Owner integration. Projects must be developed and executed with all stakeholders aligned behind the asset owner’s business goals, objectives and priorities. The best way to accomplish this is through a project leadership team deeply integrated with the owner. Traditional and non-traditional stakeholders and the integrated project management team (IPMT) must seamlessly work together. IPMTs have achieved remarkable project success, which is expected to continue globally.

- Expertise. Project leadership teams must be comprised of highly experienced, multi-disciplined project professionals who can address the nuanced complexities of a project. Critical decisions must be made promptly. Setting the design basis, understanding the technology and its requirements, and managing the supply chain are key.

About the authors

MICKEY REEVES began his 40-yr career working in U.S. refineries, where he held positions in engineering, planning and economics, operations planning, operations supervision and health, safety and environmental. He transitioned into consulting and engineering in mid-career, working on refining projects in South America, Canada, the U.S. and the Middle East. A significant part of Reeves's career was spent with Jacobs Engineering, where he worked as a Lead Process Engineer, Consultant, Process Engineering Department Manager, and Vice President of refining and petrochemicals – Middle East. In his final role at Jacobs, he was Managing Director of Jacobs Consultancy. Reeves earned a BS degree in chemical engineering from the West Virginia Institute of Technology and an MS degree in chemical engineering from the University of Houston.

REBECCA BORGH is the Marketing Director for TritenIAG. She is a strategic branding expert, designer and editor who helps brands modernize their image, launch sustainable projects and bring products to life.

CHRISTINE PORTILLO is a writer, editor and communications professional specializing in content creation and management, interactive marketing and social media. She has a strong background in engineering and technical communications for global audiences; hardware and software end-user documentation; proposal and corporate style guide development; and newspaper journalism. An English major and language lover, Portillo is committed to telling a crisp, clear and compelling story.

Related Articles

Connect with H2Tech