Articles

Scaling up fuel cells for mass adoption

Special Focus: Fuel Cell Applications

A. KNEISZ, Advent Technologies, Düsseldorf, Germany

The promise of clean energy and transportation through hydrogen (H2) has been espoused for many years. With greater energy density than other gases, H2 can be used in many applications, though the challenge is extracting it from other forms, such as water and natural gas.

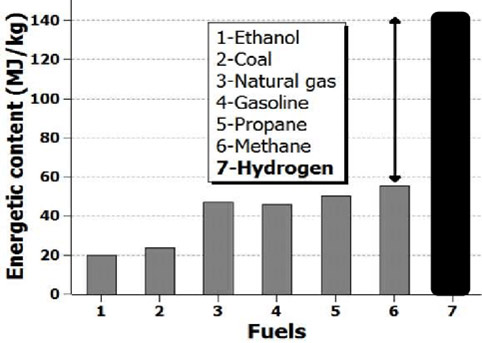

Green H2 enables the deployment of renewables by converting and storing more than 500 terawatt-hours (TWh) of otherwise curtailed electricity. It allows international energy distribution, linking renewable-abundant regions with those requiring energy imports. It is also used as a buffer and strategic reserve for power. The Hydrogen Councils vision sees H2 powering more than 400-MM cars, 15 MM–20 MM trucks and around 5-MM buses by 2050, which constitutes on average 20%–25% of their respective transportation segments, with 25% of the global CO2 abatement coming from H2 related technologies (FIG. 1).

With the billions already committed to green H2 (now projects in the gigawatt level) and decarbonization of industry using lower emissions fuels (e.g., steel and ammonia), the next step will be to use H2 in other applications such as vehicles and power applications.

What has limited this advancement over the years, as with any developing technology, has been scale. Though there was hype around 2000 for fuel cells, the technology was not ready for prime time. However, the circumstances have certainly changed, and though there are still some concerns, fuel cells are prepared for major applications.

Major innovations are ongoing, especially with polymer electrolyte membrane (PEM) technology, where an ecosystem of hundreds of companies are developing and redefining the major components and end products available in the market. For example, the author’s company is developing high-temperature fuel cells, enabling next-generation technology to reduce system costs and allow heat utilization.

Certain markets are especially central to the technology’s technical development, primarily in Canada, Europe, South Korea, Japan and, to a lesser extent, the U.S. and China. For instance, most heavy-duty fuel cells (e.g., trains, trucks and buses) are from Canada, while Japan and Korea dominate light duty.

Applications of these fuel cells in terms of deployment are heavily focused on the U.S., China and Europe, with expansion in Japan and Korea starting to move forward.

Innovation and larger production centers are being developed in those markets to scale up more extensive production facilities. Incentives for production are focused in Europe and North America, while China is pushing demand and localization strategies with incentives for end vehicles to spur the market.

Volumes are still relatively small, with a small fraction of the global market. However, there is light at the end of the tunnel, as heavy-duty transport will require fuel cells if decarbonization is to be achieved. Batteries do not have the energy density and have weight issues, especially considering 1 megawatt (MW)–3 MW are required to fast charge a large truck, which is impractical for the grid. Therefore, the ease of using H2 is the only practical solution.

Markets such as Europe, which have emission reduction goals and others, will lead to H2 deployment and fuel cell technologies. Initial incentives will be integral to enable greater adoption. For instance, China already has a subsidy scheme in place, and has had a plethora of foreign manufacturers arrive and dominate the local market.

This has driven major manufacturing leaders into China, and those companies have already set up joint ventures or local production. It has also allowed for some initial scale-up and even some automated production, which allows for lower costs.

Automated production and greater scale will be the main drives for the fuel cell market to become viable and economical. Today, most production processes are hand-made, leading to smaller quantities and higher costs.

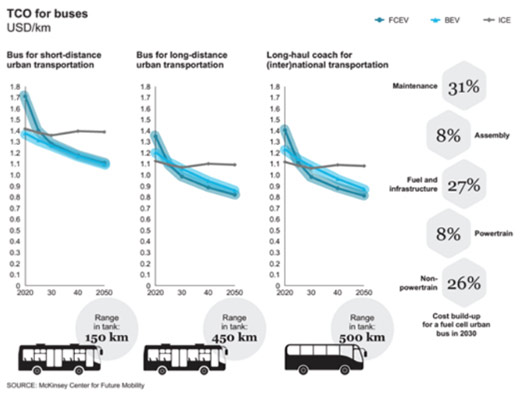

With the hope of larger bus, truck and train fleets, costs can be expected to come down levels only slightly higher than batteries on a per kilowatt (kW)/hr basis. Expectations on this reduction should be forthcoming in the 2024–2028 (depending on application) timeframe, where we can see cost parity with battery and fossil fuel technologies. Various studies have shown parity expectations on the total cost of ownership (TCO) basis, as shown in FIG. 2.

With that in mind, we can expect a large ramp-up of these technologies and major cost reductions as the ecosystem is greater and major fleets are deployed beyond China and further into Europe and North America. Larger bus and train fleets are already being deployed in China and Europe; trucks are expected to follow in the coming years.

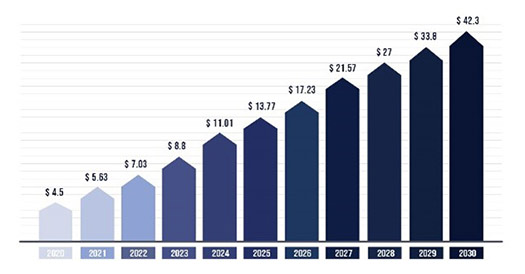

Thus, with clear projections on cost reductions and government commitments to decarbonize, extensive fuel cell scaling in markets with commitment and incentives can be expected. These markets will also benefit from carbon reductions, industrial expansion and market development (FIG. 3).

Figures are constantly being revised upwards in terms of demand and further cost reductions based on earlier estimates in the H2 industry. With the war in Ukraine and fossil fuel challenges, recent material supply and cost issues with batteries, it is hard to predict when fuel cells will be a major contributor to transportation and some power applications. The current momentum will surely see fuel cells being considered by major equipment manufacturers, fleet owners and cities as a viable alternative to battery electric and gas-powered vehicles.

The uptake with many equipment manufacturers has been slow, but that is changing. Due to slow uptake, some issues on upstarts have developed where companies have had more marketing promise than the actual product, such as Nikola and Hyzon, but this often is emblematic of a growing pain in a new industry.

Now major players are getting more involved and investing significant resources such as:

- Cummins, via the industry’s largest acquisition of Hydrogenics from Canada in 2019

- Bosch, with a recent announcement to invest $1.3 B in fuel cells by 2025

- WeChai in China purchasing part of Ballard and investing in a joint venture

- Hyundai, Toyota and BMW are investing billions via in-house programs focused on the car market

- Volvo and Daimler Truck’s joint venture investing major amounts and developing a production facility in Canada for fuel cells for heavy-duty trucks

- SK is investing in Plug Power.

These investments are significant as they are major players in traditional technology familiar with mass manufacturing, and most are automotive companies with a long history in large-scale production of similar systems. With all this large investment, it is expected that significant cost savings in components, production techniques and overall system costs will be achieved. For instance, the EU is investing billions into the development of scaling up electrolyzers (€5.5 B) and fuel cells (€782 MM). The author's company was awarded €782 MM by the EU IPCEI program to scale up manufacturing over 6 yr for a high-temperature PEM fuel cell, which allows for heat utilization and offers the ability to input other fuels such as methanol, eFuels and direct H2.

Therefore, with the growth expectations, decarbonization targets and large-scale manufacturing, the industry has a bright future to capture a large portion of the market. As the TCO gets closer to diesel and batteries in 2025 and beyond, large-scale ramp-up and mass adoption in certain sectors of the economy are expected, primarily in transportation but also in specific stationary power applications.

H2 and fuel cells are on the path to mass adoption and scale-up globally. First adopters can capture the market, jobs and economic potential of H2 fuel cells.H2T

ABOUT THE AUTHOR

ALAN KNEISZ is the Vice President of Business Development for Advent Technologies. In his role, Kneisz has been at the forefront of H2 technology deployments via significant leaders in this technology for close to 15 yr with leaders such as Ballard, Cummins (Hydrogenics) and now Advent. His experience centers around developing megawatt fuel cell power systems, renewable energy applications, energy storage, green H2 production, backup power and H2 transport solutions for trains, trucks and buses globally. Kneisz has extensive experience implementing green technologies into practical applications throughout the Asia-Pacific, Europe and Australia with private and government institutions and has become a thought leader in promoting the H2 economy across the region, speaking at approximately ten conferences per year, explaining the advantages of the H2 economy.

Related Articles

Connect with H2Tech