Articles

Sustainable ports: Learnings from an Omani ports research study

Converting Existing Infrastructure

C. ARUFFO, Dii Desert Energy, Paris, France

The ongoing energy transition is shaping a new world that will ultimately be powered by emissions-free energy. Of the impending transformations, the global supply chain—today, largely based on fossil fuels—is set to undergo fundamental changes in transport and infrastructure. The hydrogen (H2) and derivative transport markets are expected to reach up to 400 MMtpy by 2050,1 representing an excellent opportunity for ports to become central and active hubs for logistics, manufacturing and other industrial activities. Localizing new business activities in and around ports can deliver in-country value by stimulating regional and national growth and creating new job opportunities.

The author’s company recently conducted a study on behalf of ASYAD and in cooperation with the Oman Hydrogen Centre.2 The report analyses in depth the three main deep-sea Omani ports and related opportunities, providing lessons that can be applied to ports worldwide in the context of the energy transition.

Ports as H2 valleys and clean H2 hubs. H2 valleys are envisaged as integrated ecosystems that cover the entire spectrum of value chain elements, from production to final consumption. All activities—zero- and low-emissions H2 production, storage, distribution and use—are meant to be concentrated in a specific geographic area, resulting in benefits such as lower H2 costs, enhanced investment attraction and industrial localization. Therefore, ports are ideal locations to become H2 valleys and fully-fledged clean industrial hubs, provided integrated activities are planned early in the process and leverage existing assets and industries.

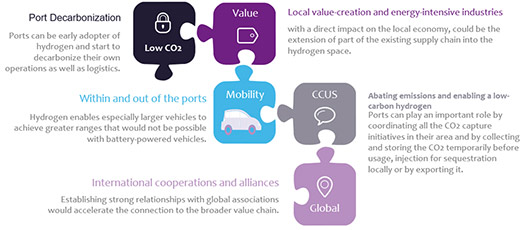

Ports would provide a great stimulus in accelerating decarbonization efforts for existing plants (e.g., refineries and steel assets already located at ports or in the vicinity). Early adoption of H2 can lower emissions and provide an important competitive advantage as the demand for clean products will soon be predominant.

Attracting new industries—especially those that are energy-intensive—directly impacts local economies and contributes to in-country value creation. Existing supply chains (e.g., dry docks, welding capabilities) can be extended wherever possible to cover the H2 space. Localizing new production facilities in or at nearby ports helps reduce H2 transport and derivatives costs. Equally important is designing an efficient infrastructure system based on repurposing existing facilities or completely new networks, depending on each country’s needs and regulatory requirements.

As high emitters of carbon dioxide (CO2), ports are well-positioned to coordinate all CO2 capture initiatives nearby. CO2 could then be stored temporarily before usage, injection, sequestration or export. Besides storing CO2, ports offer storage opportunities for different products (e.g., the bunkering of H2, derivatives) to all industries in the valley that can be complemented by underground storage in suitable, nearby locations.

While the first H2 valleys are nascent, it is important to note that some are planned around ports (e.g., the Port of Rotterdam) or connect multiple ports (e.g., the Ports of Flanders, including the Port of Antwerp-Bruges, North Sea Port and Port Oostende). Collaborations and learnings from these early experiences can stimulate similar plans on other continents. Additionally, building close cooperations with global associations like the Global Maritime Forum (GMF) can facilitate connections to the broader value chain.

Potential application for H2 at the ports. Ports are in a favorable position to lead the adoption of H2 to decarbonize operations and logistics, thus optimizing their energy efficiency and carbon footprint (FIG. 1). For the three Omani deep-sea ports, several potential applications have been identified, most of which can be replicated elsewhere:

- Logistics. Internal logistics and mobility within and out of the ports can benefit from deploying H2-powered vehicles (e.g., trucks, forklifts). Solutions to reduce carbon footprint are already available in other sectors (e.g., H2 mobility projects at airports) and can be easily applied to ports. Furthermore, low-carbon cold chain logistics development can leverage advancements in fuel cell technology for high energy-consuming vehicles like refrigerator trucks.

- Bunkering. Ports in strategic locations can aspire to become low-emissions bunkering hubs, taking advantage of the H2 derivatives trade flow’s evolving landscape. It is advisable for neighboring ports to coordinate their efforts and differentiate the offering of bunkered products to avoid competing in the same market.

- Ship refueling. With the ongoing efforts to decarbonize shipping traffic, H2 derivatives (e.g., ammonia, eMethanol) are expected to gradually replace fossil fuels. The evolution of ocean vessel engines represents an important opportunity for ports to refuel ships with low-emissions ammonia and eMethanol during the unloading and loading of goods.

- Heavy industry. Ports usually host heavy industries, such as steel and cement production. However, ammonia and methanol production requires large amounts of energy. Gradually replacing fossil fuels with H2 is an important opportunity to reduce carbon emissions and decarbonize industrial processes.

- Refineries. Many refineries are located in or near ports, producing and consuming significant H2 for crude oil desulfurization. As a first step, H2-based fuels can be blended with conventional fuels to satisfy the increasing quota of sustainable fuels required by certain industries (e.g., aviation). In this context, refineries can become enablers of clean mobility, keeping in mind that, ultimately, traditional refineries will cease to exist and will fully convert into eFuels production sites.

Shipping pathway to decarbonization. The shipping industry is responsible for 3% of global CO2 emissions—this will require important transformations in the coming years. Major operators worldwide are implementing strategies to drastically reduce carbon emissions, mostly based on adopting eFuels to meet their decarbonization targets. However, the GMF warns that targets should be supported by regulations and policies to close the gap price with fossil fuels and drive the demand for low-emissions eFuels.3 Some international regulations are already in place, such as the International Maritime Organization (IMO) requirements and European Union regulations.4 Additional standards are in development (e.g., Carbon Border Adjustment Mechanism).5 Shipping operators and ports should account for these rules, especially when exporting goods across different countries.

The demand for dual-fuel engines is rising and expected to increase to 50% by 2032 at a marginal cost of only 10%−20% higher than traditional engines. Regarding eFuels, ammonia and eMethanol are projected to reach comparable demand by 2030 and compete with liquified natural gas (LNG) for an equal market split.6 It is worth noting that, besides its use as shipping fuel, ammonia is likely to be the carrier of choice for sea transport.

Takeaway. Ports have the potential to play a crucial role in the ongoing energy transition by developing into H2 valleys and clean industrial hubs. Such clusters could serve as catalysts for developing H2 value chains, thus attracting new businesses and creating new job opportunities. Localized H2 use and processing can decarbonize port operations and reduce their carbon footprint. Several potential applications for H2 and derivatives at ports have been identified, such as decarbonizing logistics, heavy industry and refineries, as well as bunkering and ship refueling. Existing assets can benefit greatly from the early adoption of H2 in decarbonization efforts and gaining a competitive advantage as demand for low-carbon products constantly increases. H2 and derivatives will be key in facilitating decarbonization in the shipping sector. Ammonia and eMethanol are forecast to soon compete with heavy fuels in the shipping sector, provided regulations and policies are in place to help drive clean fuel demand.H2T

About the author

CHIARA ARUFFO is the Director of Research for Dii Desert Energy, a leading think tank in the Middle East and North Africa (MENA) region advocating for accelerating the energy transition. She maintains the Renewable Energy projects MENA database and the MENA Hydrogen Tracker with Roland Berger. Dr. Aruffo earned a PhD in CO2 storage and has several years of industry experience, notably at Shell, with office-based and operational roles. After Shell, she ventured into digitalization and machine-learning with a startup before joining Dii Desert Energy. As a side project, Dr. Aruffo co-founded and managed Sportopolis.it, an online sports magazine with a broader focus on sustainability and the energy transition in sporting events.

LITERATURE CITED

1 McKinsey & Company, “Global hydrogen flows: Hydrogen trade as a key enabler for efficient decarbonization,” October 2022, online: https://hydrogencouncil.com/wp-content/uploads/2022/10/Global-Hydrogen-Flows.pdf

2 Dii Desert Energy, OHC, ASYAD, “The potential role of ports in Oman in the clean hydrogen transition,” 2022, online: https://dii-desertenergy.org/wp-content/uploads/2022/12/asyad_hydrogen-report_2022-1.pdf

3 Getting to Zero Coalition, “The next wave green corridors,” November 2021, online: https://www.globalmaritimeforum.org/content/2021/11/The-Next-Wave-Green-Corridors.pdf

4 European Commission, “Reducing emissions from the shipping sector,” online: https://climate.ec.europa.eu/eu-action/transport-emissions/reducing-emissions-shipping-sector_en

5 Smith. R., “Hydrogen regulations by jurisdiction and changing transmission systems,” June 2022, online: https://www.reedsmith.com/en/perspectives/energy-transition/2022/06/hydrogen-regulations-by-jurisdiction-and-changing-transmission-systems

6 MAN Energy Solutions, “Methanol engines continue rise with major order,” October 2022, online: https://www.man-es.com/company/press-releases/press-details/2022/10/18/methanol-engines-continue-rise-with-major-order

Related Articles

Connect with H2Tech