Articles

Six steps for driving the H2 economy with digital technology

Digital Technologies

R. BECK, AspenTech, Boston, Massachusetts

There is significant interest and a corresponding level of innovation activity in the key opportunity areas of the hydrogen (H2) economy. These opportunity areas include green and low-carbon H2 production, storage and delivery to market, carrier fluids and end uses (e.g., fuel cells and H2/natural gas mixtures). These areas of opportunity are driving major investments in the sector as well as global capital project activity. However, hurdles persist.

In his recent book on climate solutions and breakthroughs, Bill Gates talks about the “green premium.”1 In other words, the world must pay more for green energy, and the extra cost must be eliminated. Gates argued that through trillions of dollars of investments, innovation and breakthroughs will accelerate, reducing and eliminating the green premium. For H2, those levels of investment are expected. Today, H2 activity is being jump-started through government incentives, favorable regulations, taxes and research subsidies. The U.S. Department of Energy (DOE), through the Inflation Reduction Act, is providing multiple billions towards moving green H2 toward economic parity as an energy source.

According to a report by McKinsey and Company, H2 is expected to account for 20% of global carbon abatement by 2050.2 According to a May 2022 analysis by H2Tech, there are 930 H2 projects globally, 47 of which the Hydrogen Council calls giga-scale projects. Today, the world’s H2 production is approximately 100 MM metric tpy. The majority is for captive use in refining and chemical processes. The World Bank projects the number will grow by more than 9%/yr through 2030, with global H2 production reaching 500 metric MMtpy–680 metric MMtpy by 2050.3

This sounds good, but why are some of the largest initiatives developing so slowly? As long ago as 2003, the U.S. and Europe agreed to collaborate on accelerating the H2 economy, but it is finally becoming a reality. What are the remaining hurdles to scaling up the global H2 value chain and realizing the projects from the World Bank, Hydrogen Council, International Energy Agency, McKinsey and others?

The biggest hurdles are the economics of H2 production, delivery and use. According to the International Renewable Energy Agency (IRENA), H2 energy is 2–3 times more expensive than fossil energy (not counting the carbon cost), and H2 pipelines are 10%–50% more expensive than natural gas and oil pipelines.4

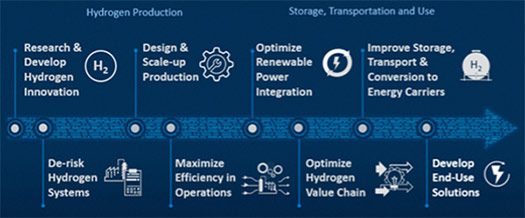

Digital technologies will provide the magic bullet that will level the playing field, and it can do so quickly for the players who embrace it. The author’s company has developed a sustainability pathway for the H2 economy that makes the key digital technologies easy to adopt for supporting the innovation, execution and scaling of H2 projects across the value chain, from renewables to H2 production to storage and delivery of H2 to end use (FIG. 1).

Six steps to adopting digital technology in the H2 economy are discussed here:

- Systems-level analysis of a H2 project: Defining the best choices in the investment stage of H2 projects is complicated due to many alternative pathways, technology choices, new technology risks and weather variability. Making the right choices to balance scale, risk and innovation will be one of digital technology’s greatest impacts. The author’s company has built a H2 economy sample model into its risk and availability system’s analysis system, working with several groups that are at the early stages of large H2 projects to help take a fact- and risk-based approach to making technology, configuration, location and process decisions at the earliest project stages.

- Digital twin modeling of H2 production to reduce capital costs by 75%: Digital twins are an effective tool in proven industrial areas. In the H2 economy, digital twins are an essential engineering, estimating and project tool that will enable:

- The evaluation of thousands of alternative design choices to select the leading candidates regarding productivity and efficiency, and also optimize the overall process beyond the core technology components (such as electrolysis)

- Rapid evaluation of costs and economics related to alternatives

- Virtual mirroring and constant performance evaluation of new technologies, such as electrolysis systems for green H2 and integrated reforming and carbon capture and storage (CCS) systems for low-carbon (blue) H2

- Ongoing feedback of early operating modules and improvement of future modules.

For H2, digital twin feedback will be crucial in the expected progressive implementation strategy. Digital twins provide uniquely accurate and complete modeling approaches for green and blue H2 (electrolysis, reforming, ammonia production and associated carbon capture). The author’s company is working with Emerson Electric to link its rigorous models with Emerson’s operator training (OTS) digital twin and augmented reality operator training, which will accelerate training and H2 startup projects. Air Products has published a case study describing the use of digital twin models across its network of H2 plants and pipelines throughout the U.S. Gulf Coast. That case study documents more than $1 MM/yr in operation cost reduction, as measured in one of the 15 plants managed with the help of these models.

- Optimization of renewable power, storage and electrolysis to increase H2 production load factor and reduce operating costs by 10%: Much of the focus on the capital costs is associated with H2 electrolysis; however, reducing the operating costs for H2 production is also crucial. Distributed energy resource management (DERMS) and microgrid solutions can optimize renewable power arrays with power storage, optimizing power delivery for electrolysis and carbon capture. DERMS and microgrid solutions combined with software that optimizes power utilization in processes such as green and blue H2 production provide a comprehensive opportunity to reduce energy-based operating costs by 10% or more. This approach has attracted considerable interest from several H2 projects in the design stage.

- Monitoring, measuring and modeling H2 storage and transport for safety to achieve 100% availability: Dr. Robert Socolow, co-author of the 2003 Hydrogen Economy Blueprint, believes that safety is an important concern for the rapid adoption of the H2 economy for H2 delivery and end use.5 Modeling solutions can rigorously model the behavior of low-temperature H2, ensuring safety envelopes in the system’s engineering. A pipeline monitoring and management solutiona will provide operational awareness of the reliability and integrity of transport systems. Emerson Electric is linking the rigorous models with its advanced measurement technology to monitor, detect and prevent H2 leaks.

- Optimization of the H2 value chain: The overall economics of H2 will depend on a value chain that, in most cases, will cross multiple company boundaries. A planning solutionb is an ideal tool to design and manage the various pathways along H2 value chains. In conjunction with systems-level modeling (described in the first bullet above), these two digital solutionsa,b will enable H2 economy players to make the correct investment decisions across the H2 economy, in process technology selection and regarding value chain paths (e.g., pipelines, carrier fluids).

- Improvement and optimization of H2 end use for economics and safety to ensure market acceptance: The same rigorous and accurate models used for H2 electrolysis technology innovation also provide high value in the innovation and engineering stages for scaling the H2 fuel cell market. Doosan Fuel Cell is only one of more than 15 fuel cell and automotive companies using the author’s company’s process modeling in fuel cell engineering activities. Digital twins will be crucial in accelerating the improvement of fuel cells from version to version as usage increases.

Takeaway. Digital technology is already—and will continue to be—a strategic element in reducing cost across the H2 value chain, accelerating the scaling and speed of implementation, and ensuring the safety and reliability of H2 solutions. Discussions and workshops between organizations are necessary to accelerate efforts and opportunities in the H2 market.H2T

Notes

a AspenTech OSI Continua

b Aspen Unified PIMS

LITERATURE CITED

1 Gates, B., “How to avoid a climate disaster,” Alfred A. Knopf, 2021.

2 McKinsey and Company, “Hydrogen’s potential in the net-zero transition,” May 2023, online: https://www.mckinsey.com/~/media/mckinsey/email/rethink/2023/05/2023-05-10d.html#:~:text=Our%20work%20with%20the%20Hydrogen,a%20%24460%20billion%20investment%20gap

3 World Bank, “Green hydrogen: A key investment for the energy transition,” June 2022, online: https://blogs.worldbank.org/ppps/green-hydrogen-key-investment-energy-transition#:~:text=The%20demand%20for%20hydrogen%20reached,680%20million%20MT%20by%202050

4 IRENA, “Hydrogen,” 2022, online: https://www.irena.org/Energy-Transition/Technology/Hydrogen#:~:text=Hydrogen%20is%20produced%20on%20a,of%20a%20mix%20of%20gases

5 U.S. White House, “Hydrogen economy fact sheet,” June 2003, online: https://georgewbush-whitehouse.archives.gov/news/releases/2003/06/20030625-6.html

About the author

RON BECK is the Senior Director of Solutions Marketing at Aspen Technology. He works with global energy and chemical companies on digitalizing sustainability and decarbonization pathways. Beck has more than 40 yr of experience in the intersection of the energy industry, digital technology and environmental science. His work in sustainability and energy security goes back to the first U.S. energy crisis in 1973 and 1974 when he was involved in the U.S. DOE strategy work and innovation, including conducting one of the first economic studies of wind energy, waste conversion through pyrolysis and new approaches to enhanced oil recovery.

Related Articles

Connect with H2Tech