Articles

UK-Germany H2 corridor: Pie in the sky or breakthrough?

Special Focus: H2 Mobility, Pipelines and Transportation

A. WALSTAD, Contributing Author, London, UK

Germany and the UK have outlined ambitious plans for a large-scale hydrogen (H2) network between the two countries, and this is at a time when the sector is faced with growing pessimism.

In May 2025, National Gas, the operator of Great Britain’s National Transmission System (NTS) for gas, signed a memorandum of understanding (MoU) with Germany’s GASCADE to explore the feasibility of a H2 pipeline between the two countries.

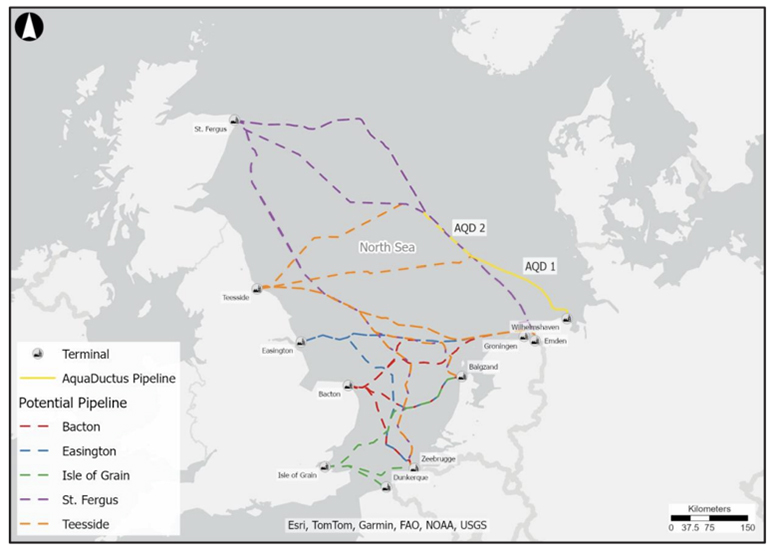

The UK-Germany Hydrogen Corridor would provide transport capacity for up to 20 GW of H2 and operate on a bi-directional basis, according to plans. The project includes offshore pipes that would start in either Teesside in northeast England or St Fergus in Scotland. St Fergus, near Peterhead in Aberdeenshire, is home to a large gas processing terminal, while Teesside aims to become the UK’s first decarbonized industrial cluster by utilizing carbon capture and storage (CCS) and H2.

The UK pipeline would tie up with GASCADE’s AquaDuctus pipeline project in the North Sea and therefore link up with mainland Germany and the continent (FIG. 1).

A recent feasibility study published by London-based Arup Group found that pipeline route options from the UK to AquaDuctus are technically feasible “at a high level.” It would, however, require further assessment and more certainty on how the two countries’ domestic networks will materialize in the next decade.

Conversely, the study also said converting existing interconnectors and pipelines in the North Sea to transport H2 looks unlikely—at least in the short to medium term—due to existing gas supply contracts and security of supply considerations.

H2 of all colors. The UK-Germany corridor could be filled with both blue H2 (natural gas + CCS) and renewable H2 produced by wind power, thus connecting production sites in the UK with demand centers in Germany, and perhaps vice-versa. However, while transmission system operators (TSOs) are jointly engaging with H2 producers and end users as part of the MoU signed in May, no firm offtake agreements have been secured yet, according to National Gas.

As for the AquaDuctus pipeline in the German North Sea that is being developed by GASCADE and Fluxys, the plan is to connect the first large-scale H2-producing offshore wind farm, the 1-GW capacity SEN-1 project northwest of Helgoland, by 2030. A 200-km section of the pipeline will transport the green H2 onshore to Germany and further on, through an existing 100-km network, to the German-Netherlands border. In the next project stage, AquaDuctus will be extended by another 200 km to the remote areas of the German North Sea where, if successful, ~1 MMtpy of green H2 will be produced by offshore wind farms with a combined installed power generation capacity of 10 GW.

As a potential cross-border project, AquaDuctus has been classified as an Important Project of Common European Interest (IPCEI), which means it could benefit from increased state funding than would otherwise be allowed under EU state aid rules. In addition to the UK, there are also ideas to connect the pipeline with the Netherlands, Belgium, Denmark and Norway.

The German section of the pipeline is also considered a Project of Common Interest (PCI), which means it could benefit from faster permitting and perhaps EU funding.

Reality check. The announcement concerning the UK-Germany corridor comes as the H2 sector is experiencing a period of growing pessimism, with many projects shelved due to high costs and lack of end user commitment.

However, there are reasons to believe the UK-Germany corridor has the potential to be an industry breakthrough. The UK, for its part, is advancing projects for CCS and blue H2, including the aforementioned Teesside project as well as other projects such as Humber in northeast England and Hynet NorthWest, which spans across Liverpool, Manchester and north Wales. The UK also has about 15 GW of installed offshore wind capacity and has set an ambitious target to reach 43 GW–50 GW by 2030.

Meanwhile, Germany still has a strong industrial base that must be decarbonized, and the country has begun rolling out a domestic grid for H2 transport. This includes ambitious plans for a 9,040-km H2 pipeline network that could be completed in 2032 at a cost of ~$20 B.

Work on the H2 network has begun. In April this year, Ontras, the TSO in eastern Germany, said it had completed the Bad Lauchstädt Energy Park, a converted, 25-km gas pipeline to connect the electrolyzer under construction at the TotalEnergies refinery in Leuna. The pipeline will initially be filled with natural gas and H2 at a later stage.

Climate targets are hard to ignore. Moreover, for Germany to reach the target of climate neutrality by 2045, H2 would be a necessary component.

Lucas Sens, a Senior Energy Market Analyst for Power and Hydrogen at Energy Exemplar, who is expressing his own views and not speaking on behalf of his employer, said, “If we want to reach climate neutrality, we will need H2. Similar to the Pareto principle, the first 80% of defossilization is likely to be achieved cost-effectively without H2. But for the remaining 20%—typically the hard-to-abate sectors—H2 should play a key role. Based on the studies I have seen and considering all circumstances, I assess that green H2 is the option with lower overall system costs in the long term compared to blue H2.”

Yet high costs compared with conventional fuels means early optimism concerning the scale of H2 production has been fading.

“Three to four years ago, we had a H2 hype, and in nearly every energy application, H2 was seen as a viable option. Right now, we can see a market consolidation, and in several areas, other technologies such as battery electric passenger vehicles or heat pumps have cost advantages. Therefore, the focus is now shifting to hard-to-abate sectors. Examples would be in aviation and shipping where H2 and its derivatives are promising energy carriers or industrial applications where H2 is needed as an inherent feedstock,” said Sens.

EU funding, but how many billions? Rolling out pipeline and network infrastructure seems fundamental to get the H2 economy going. To this end, the European Commission has proposed almost €30 B in funding for energy infrastructure, including H2 projects under the Connecting Europe Facility (CEF) from 2028–2034. That is an increase from around €6 B in funding under CEF from 2021–2027.

As an essential tool to complete the Energy Union, the EC says the CEF will provide funding to energy infrastructure projects in the electricity, H2 and carbon dioxide (CO2) transport sectors that have a significant cross-border impact and have been awarded the status of a PCI or Project of Mutual Interest (PMI) under the Trans-European Networks for Energy Regulation (TEN-E Regulation).

As for other funding mechanisms, the EC has also proposed an Industrial Decarbonization Bank, aiming for €100 B in funding, based on available funds in the Innovation Fund, additional revenues resulting from the EU’s Emissions Trading System (ETS) as well as the revision of InvestEU.

Additional funding will be sorely needed as H2 infrastructure is not cheap. However, with political priorities in the EU and in many European capitals ostensibly shifting from climate to industrial competitiveness and defense, support should not be taken for granted.

“In comparison to batteries, photovoltaics and wind power, H2 still needs significant funding to become economically viable, as it excels particularly in large-scale systems. Looking at the political landscape and the current challenges, I hope that the European Union and its member states have the willingness and capacity to launch effective and unbureaucratic funding schemes,” said Sens.

Despite the risks and upfront costs, investing in a H2 network now could pay off.

“If we want to quickly develop a H2 market, a backbone pipeline system for H2 transportation is crucial to kickstart the market, helping to match H2 supply and demand with low specific transportation costs. It is a big investment with relatively high risk in terms of demand realization, but over time, the transportation costs using a pipeline network are much lower compared to, for example, transporting H2 by truck,” said Sens.

Energy security boost. A cross-border H2 network will bring many benefits, Sens adds. “In terms of minimizing system costs, generally speaking, an interconnected energy system between countries is always beneficial. It provides more options for a cost-effective alignment of supply and demand, especially when green H2 production relies heavily on inconsistent energy sources like wind and solar.”

Although the UK-Germany H2 corridor must overcome many hurdles before it becomes a reality (e.g., commitment from H2 buyers and suppliers), the MoU shows that there is still willingness to develop large-scale projects across borders. The EU has agreed to sanction Russian LNG imports with full effect from the beginning of 2027 and is currently discussing a ban that would also include pipeline gas. This means the business case for H2 could be strengthened as it could help replace some of these Russian gas volumes.

Ulrich Benterbusch, Managing Director at GASCADE, said at the signing ceremony at the World Hydrogen Summit in Rotterdam in May: "Through joint infrastructure projects like this, we can leverage the UK's significant renewable resources and Germany's strategic H2 storage and consumption capabilities, diversifying energy imports and strengthening European energy security." H2T

About the author

ANDREAS WALSTAD has written extensively about natural gas and energy issues for two decades. He divides his time between London and Brussels and also regularly attends conferences around Europe. Walstad holds university qualifications in journalism and economics. Outside of work, he is an avid kayaker. The author can be reached at andreas.walstad@gmail.com.

Related Articles

Connect with H2Tech